We’ve spent the last few years doing what a lot of people now call “location-independent living” — moving between countries like Thailand, Malta and China, sometimes for a few weeks, sometimes for several months, and occasionally longer. It’s a lifestyle that looks easy from the outside. But the longer you do it, the more you realize that some things — like health insurance — are anything but simple.

Because the reality is: you never know what can happen, and you rarely know what it will cost. A minor clinic visit in one country can turn into a serious expense in another. And what makes it harder is that you often don’t really know if you’re covered until the moment you actually need it. Many policies look fine on the surface, but once you get into the fine print — 30, 60, 90-day limits, exclusions, conditions — it quickly becomes less about coverage and more about interpretation.

In the end, it comes down to trust. Finding companies that are built to support you when something goes wrong — not just to sell another monthly subscription.

With that in mind, we decided to take a closer look at Genki, one of the newer insurance providers focused specifically on digital nomads. We tested their pricing calculator based on our own situation — already abroad, moving between countries — to see what it actually costs and what’s included. And we spoke directly with the team behind Genki to understand how their approach differs from more traditional insurance models.

A Few Words About Genki Insurance

Genki is a Cologne-based health insurance provider (an online platform) built for digital nomads, remote workers, and long-term travelers. It offers worldwide coverage without needing to declare your destination, so you can move freely between places like Thailand, Bali, or Europe and stay continuously covered.

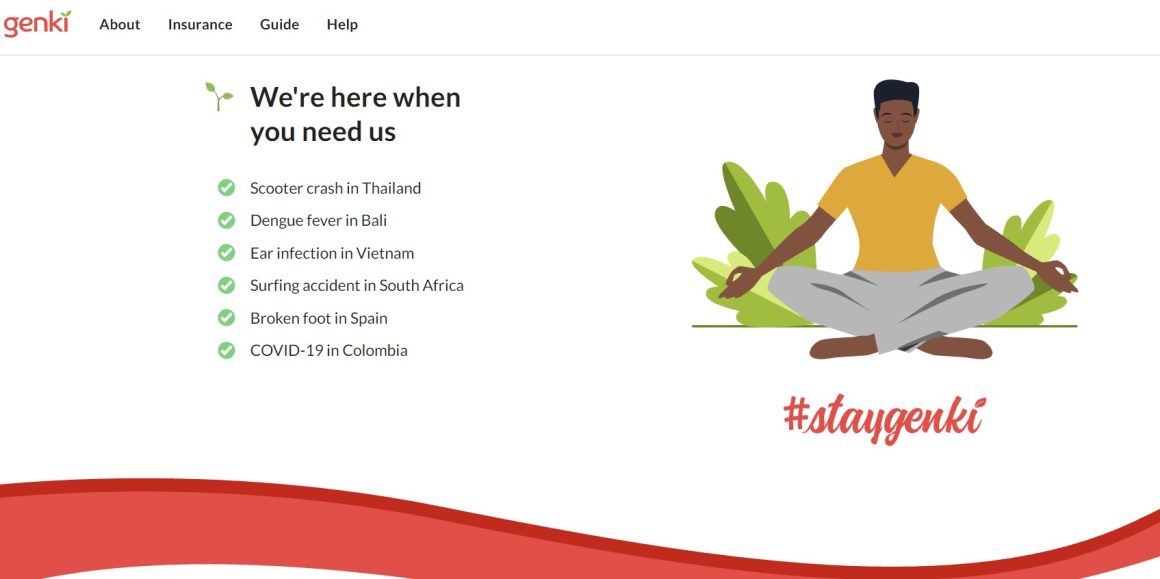

The focus is on real-life healthcare abroad, not just worst-case scenarios. That means you’re covered whether it’s:

- a scooter crash in Thailand

- dengue fever in Bali

- an ear infection in Vietnam

- a surfing injury in South Africa

- or even a broken foot in Spain

Genki covers necessary medical treatment worldwide, with access to any licensed doctor or hospital, plus a 24/7 emergency hotline. In serious cases, hospitals can contact Genki directly and get paid without you handling the bill.

For everyday visits, it’s simple: see a doctor → submit your claim → get reimbursed (often within ~2 weeks).

The setup is designed to be frictionless:

- No home country requirement

- No need to update your location

- Sign up online in minutes, even if you’re already abroad

- Flexible monthly coverage for travelers on the move

Two main plans:

- Genki Traveler — flexible travel health insurance (up to 12 months)

- Genki Native — long-term international health insurance with broader coverage

In short, Genki is built for people whose lives don’t stay in one place — and who need health insurance that works just as globally as they do.

“Insurance Is Just the Starting Point”

Unlike traditional providers, Genki did not begin with actuarial models or legacy systems. It began with a gap — one that becomes obvious the longer you live without a fixed address.

“We’re a bunch of nomads ourselves, so we made Genki for us — and people like us,” says Neville, co-founder and head of marketing. “We didn’t start with the idea of being an insurance company.”

Founded in 2021, the Cologne -based company now covers more than 75,000 members across 195 countries. It positions itself less as a traditional insurer and more as a layer of infrastructure for a lifestyle that doesn’t fit neatly into national systems.

“Health goes well beyond insurance. Insurance is just the starting point.”

That framing reflects a broader shift. Remote work, once temporary or experimental, has become long-term for many. But the systems that underpin it — healthcare, insurance, residency — are still largely built for people who stay in one place.

A Lifestyle That Doesn’t Fit the System

Most insurance products assume stability: a home country, a return ticket, a defined timeline.

Digital nomads tend to have none of those.

“One of the biggest challenges is understanding what type of insurance actually fits your lifestyle,” Neville says.

Travel insurance, in its traditional form, works well for holidays. It covers cancellations, lost luggage, and some emergency care. But it is built around a start date and an end date.

Many long-term digital nomads no longer operate that way.

“Travel health insurance can be great while you’re abroad — but it’s not meant to be your only healthcare cover.”

The result is a gap between how people live and how they are insured — one that often only becomes visible when something goes wrong.

When Flexibility Becomes a Risk

The appeal of the lifestyle is obvious: the ability to move between Bali, Lisbon, or Mexico without long-term commitments.

But that same flexibility can create problems.

“If you get local insurance in one country, you can’t take it with you,” Neville says. “And if you develop a condition during that time, it could become a pre-existing condition.”

It is the kind of detail that rarely features in marketing material, but becomes decisive when trying to move on — geographically or medically.

The Fine Print That Matters

Insurance policies tend to look similar on the surface. The differences emerge in the conditions attached to them.

Genki points to a handful of issues that repeatedly catch travelers off guard:

- How long does coverage actually last

- limits on treatments and reimbursements

- exclusions for sports such as surfing or diving

- restrictions on scooters and motorcycles

- The limits of bundled insurance from banks or credit cards

“We’ve met plenty of travelers who think they’re covered through their bank or credit card,” Neville says. “It can be useful — but it’s usually limited to 30 or 90 days.”

In parts of Southeast Asia, where scooters are the default mode of transport, exclusions like that are not theoretical. They shape how — and whether — a policy works in practice.

Rising Costs, Fewer Assumptions

For years, one of the quiet advantages of living abroad was cheaper healthcare. That assumption is becoming less reliable.

“Private healthcare in places like Thailand or Mexico is already quite expensive — and prices keep rising,” Neville says. “In some cases, surgery can cost more than in Europe.”

As demand increases in popular nomad hubs, the gap between local and international pricing continues to narrow. The idea of “cheap treatment abroad” is no longer something to rely on.

A Model Built Around Movement

Genki structures its offering around two products.

The first, Genki Traveler, is a flexible travel health plan designed for periods of up to 12 months, with a monthly subscription model that can be canceled after the first month.

The second, Genki Native, is a longer-term international health insurance product intended to replace local coverage entirely, with broader benefits and optional add-ons.

Both are built around global coverage, rather than a single country or region — a reflection of how their users actually move.

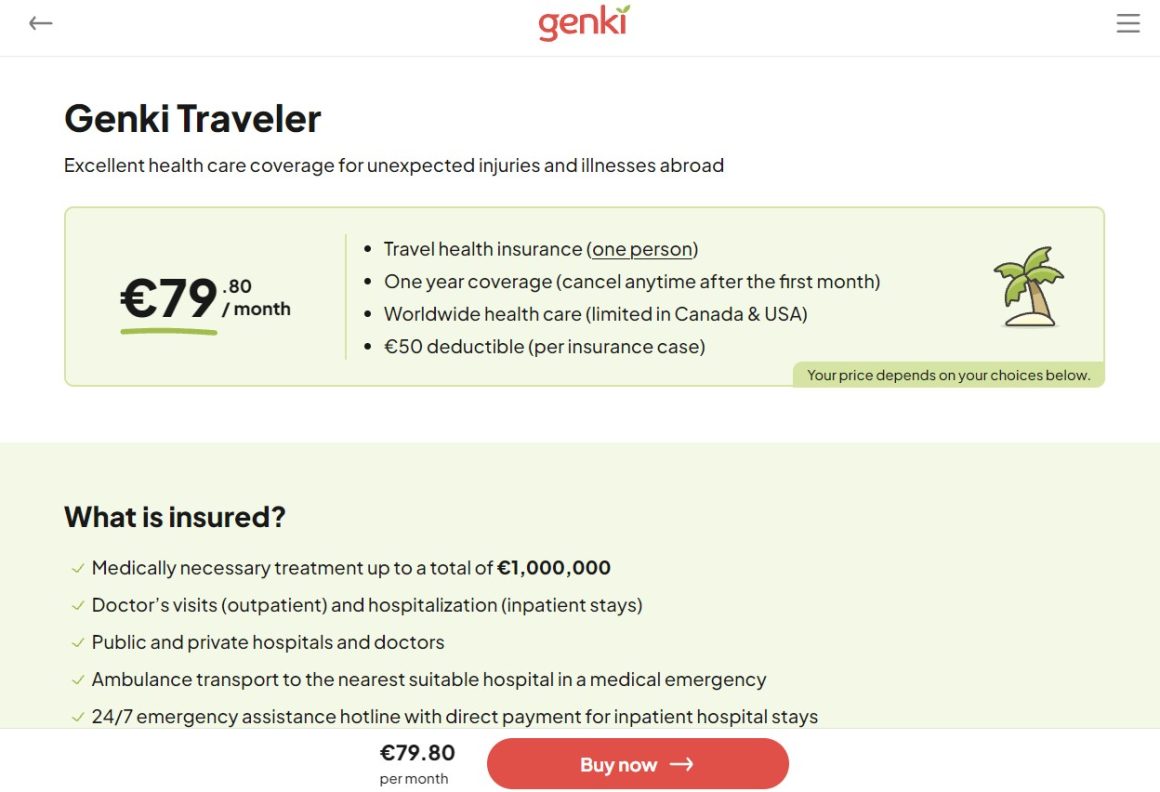

What €79.80 a Month Buys

The result is Genki’s Traveler plan at €79.80 a month.

At that level, the policy includes up to €1m in medically necessary treatment worldwide, covering both outpatient care — doctor visits, diagnostics, prescriptions — and inpatient treatment such as hospitalization or surgery.

Users can visit any licensed provider globally. In more serious cases, a 24/7 assistance line can arrange direct payment to hospitals. For routine claims, reimbursement is typically processed within a couple of weeks.

There are, however, conditions. A €50 deductible applies per case. For those already abroad without prior insurance, the first 14 days are limited to emergency treatment. Coverage in the US and Canada is limited to emergencies that begin within the first 7 days of arrival — full coverage requires upgrading to a higher-priced plan configuration. In the policyholder’s home country, coverage is restricted to short emergency visits.

What the plan provides, in effect, is a portable safety net — designed for unexpected illness or injury, rather than comprehensive long-term care.

When Something Goes Wrong

Insurance becomes real at the point of use.

“If you’re in the hospital, contact your insurance provider as soon as possible,” Neville says.

For more routine cases, the advice is simpler.

“Get all your paperwork before you leave the doctor’s office.”

It is procedural, but essential — the difference between a straightforward claim and a delayed one.

Digital Nomads – A Lifestyle That Stuck

Perhaps the most telling shift is not in insurance, but in behavior.

“A lot of people start traveling for six months — and then it turns into years,” Neville says.

In the early stages, many rely on their home country for healthcare — scheduling checkups or treatment during visits back. Over time, that approach becomes less viable.

The longer people stay abroad, the more they look for systems that match the reality of their lives — not temporary fixes, but something closer to continuity.

Insurance is one of those systems. And companies like Genki are attempting to reshape it — not for short trips, but for people who no longer live in one place.