Before I moved abroad, I needed an online bank that actually worked internationally – lower currency exchange fees, faster transactions, fewer surprises.

There are many online banks, but I signed up for the most popular Wise and Revolut. Yes, both of them. I wanted to test them side by side. Both do the job, but they feel very different.

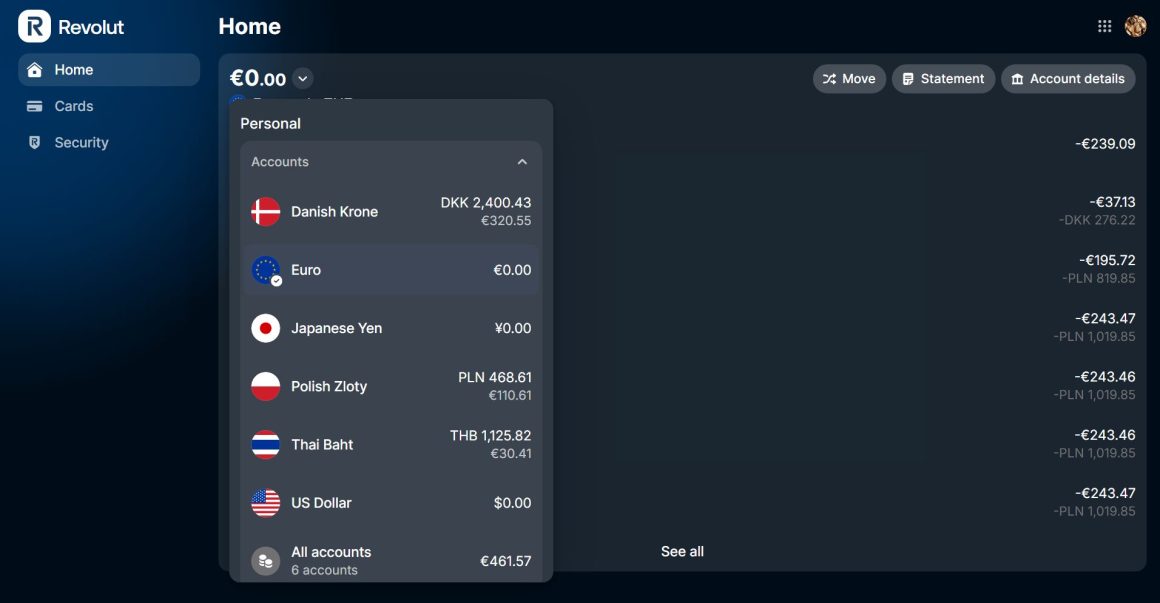

Revolut feels like a fully fledged digital bank. It has everything you expect – plus more. Trading, stocks, crypto, an eSIM, subscription bundles, tiered benefits depending on your plan.

I use Revolut Ultra. It gives me lounge access, travel insurance for up to three months at a time, and fee-free withdrawals up to €2,000 per month. In practice, it almost replaces a credit card – even though it is technically a debit card.

They also bundle services like VPNs (NordVPN), Financial Times, Perplexity, esim services and others. If you would pay for those anyway, it makes sense. If not, they are just extras.

Wise is different. It is more of a utility. I paid around €7 for shipping the card, and there is no monthly subscription. It does not try to be a lifestyle product. It just focuses on moving money at low cost.

How Online Banks Really Charge You: Fees, Exchange Rates, Subscriptions

Where Wise and Revolut really differ is in how they make money on us, users.

With Wise, every currency exchange is done at the mid-market rate – the same rate you see on Google – and then they add a clearly visible fee before you confirm.

Depending on the currency, that fee is usually somewhere around 0.4% to 1%. You see it. You accept it. That is the model. No subscription, no bundled perks – just transparent pricing per transaction.

Revolut works differently. On paid plans like Ultra, weekday exchanges are done at the interbank rate without the additional markup that lower plans charge. On free plans, weekend exchanges usually include a small percentage fee. On the Ultra plan, that weekend markup is generally removed.

So instead of paying per conversion, you are paying a fixed subscription – around €55 per month. Over a year, that is about €660.

At that point, the question becomes personal: am I using this enough to justify it? I used to be in the tier below (€100 or so a year), but with my travel activity, it made sense to upgrade, at least in the short term.

Withdrawals are another difference. Wise gives two free withdrawals up to €200 per month. After that, small fees are charged.

Revolut Ultra allows up to €2,000 per month without additional withdrawal fees, though ATM operators may still charge local fees. If you send time in cash-loving countries, it could make sense to use Revolut for this.

There is also a regulatory distinction. Revolut operates as a licensed bank in the EU, with deposits protected up to €100,000. At Wise, the guarantee is smaller and more difficult to understand, so I am trying not to keep all my savings in either place.

In daily use, both feel safe, and I use both.

Revolut and Wise – Living With Both

In practice, I use both Revolut card and Wise differently.

Revolut feels like a financial ecosystem. It replaces travel insurance. It gives lounge access. It works like a debit card but behaves almost like a premium credit card in terms of perks.

Wise feels like infrastructure. It is the tool I trust when I want clean, transparent currency conversion without thinking about subscription math.

If you move abroad or live as a digital nomad, you eventually realise the decision is less about which bank is better – and more about how you live.

If you travel constantly, withdraw cash often, and want bundled perks, a premium Revolut plan can make sense. It also helps with those Euronet ATMs that try to add a 10–15% markup when you withdraw abroad.

With Revolut and Wise, I either already have the local currency in my account, or the exchange happens inside the app at their rate. So the machine’s inflated conversion simply doesn’t get a chance. With the traditional banks I have used, this is not an option.

If you mostly want low-cost international transfers and transparent exchange rates, Wise is often enough.

Both do the job. They just solve different problems.

My Verdict: Wise Is Better for Most People, Revolut Ultra Wins for Heavy Travellers

So, if you want the best value and most honest pricing, Wise is usually the better choice – it’s the simplest, most transparent way to move money internationally without subscription maths or hidden weekend markups.

But if you travel constantly, withdraw cash a lot, and actually use the bundled perks (insurance, lounge access, eSIM, FT, VPN, etc.), Revolut Ultra can be “better” in real life, because it works like a premium travel card that replaces multiple services.

In other words: Wise is the smarter default, Revolut is the better upgrade for heavy travellers.

Revolut vs. Wise Compared

| Feature | Wise | Revolut |

| Established Date | January 2011 | July 2015 |

| Memberships | Free to open (pay-per-use utility model). | Tiered subscriptions: Standard (Free), Plus, Premium, Metal, and Ultra (~€55/month). |

| Fees | Mid-market exchange rate + 0.4%–1% clearly visible markup. €7 physical card shipping. 2 free ATM withdrawals up to €200/month. | Fixed subscription fees. Free plans have weekend exchange markups. Ultra has no weekend markup and fee-free withdrawals up to €2,000/month. |

| Benefits | Clean, transparent, low-cost international transfers. Acts as essential financial infrastructure. | Full digital banking ecosystem. Includes trading, stocks, crypto, and eSIM capabilities. |

| Perks | Local account details in multiple currencies to receive money like a local. | Partner bundles on higher tiers (NordVPN, Financial Times, Perplexity), unlimited airport lounge access. |

| Insurance Max | N/A (Not offered). | Up to £10,000,000 / €10,000,000 for global medical emergencies. Ultra tier covers trips up to 90 days. |

| License | Electronic Money Institution (EMI). Funds are safeguarded rather than bank-insured. | Licensed bank in the EU. Deposits are protected up to €100,000. |

| Legal in Countries | Supported in 160+ countries (including the UK, EEA, US, Australia, Singapore, Japan, Thailand, etc.). | Supported in the EEA, UK, US, Australia, Brazil, Japan, New Zealand, Singapore, and Switzerland. |

| Customer Support | Comprehensive Help Center, email, chat, and 24/7 phone support. | 24/7 in-app chat (100+ languages), automated phone line to block cards, and priority callbacks for top tiers. |

What Do Real Customers Say: The Good and the Bad

Customers consistently praise Wise for its unwavering transparency, loving that the exchange rate matches exactly what they see on Google without any hidden weekend markups or subscription traps. It is widely viewed as the most reliable, low-cost utility for moving money across borders.

Revolut, on the other hand, wins massive points for its sleek, “super app” ecosystem. People rave about its frictionless peer-to-peer payments, built-in budgeting tools, and premium perks like lounge access and travel insurance that easily pay for themselves for frequent travelers.

However, verified reviews for both platforms highlight a shared, major frustration: aggressive automated security systems paired with notoriously slow customer support. Because both operate as lean tech companies rather than traditional brick-and-mortar banks, their algorithms frequently freeze money accounts or block transfers for unexpected compliance checks.

When this happens, customers on both Wise and Revolut online banking apps complain about getting stuck in tedious verification loops or automated chatbot dead-ends, making it incredibly stressful to reach a real human when their money is on the line.

Revolut and Wise Online Banking Alternatives in Europe

Revolut and Wise are not the only serious players in Europe.

N26 is a licensed German bank with EU deposit protection up to €100,000. The app is clean and minimal, and for everyday euro banking it works extremely well. It also had more requirements when signing up compared to the other apps I tested.

Other newcomers include Bunq from the Netherlands, which targets digital nomads, and Monese, which promotes fast account setup with fewer residency barriers.

The differences are structural – subscription versus pay-per-use, ecosystem versus utility, banking license versus safeguarded funds.

While living in Malta, almost everyone had a Revolut account. It became the default way to pay bills, send rent deposits, or transfer money instantly between friends. If most people around you use the same app, transfers become frictionless. No IBAN typing, no waiting, no explaining which platform you are on.

In other countries, the dynamic can be different. People often lean toward digital banks with domestic licenses because there is psychological comfort in something regulated at home. Local trust plays a bigger role than fee structures.

But this is also where legacy systems show their limits.

I had to delete my MobilePay account when I was no longer a resident in Denmark. It works perfectly — as long as you live within the system it was designed for. The moment you change residency, it stops being an option.

Traditional banking systems are still largely built around domestic customers. If you stay local, they are seamless. If you move countries – short- or long-term – you often fall outside the framework.

That is where apps like Revolut and Wise still have an advantage. They are built for mobility from the start.

Through the European Mobile Payment Systems Association (EMPSA), national mobile payment providers such as MobilePay, Bizum, and Bancomat are working toward enabling cross-border instant payments between their users. That may make transfers easier between countries.

But it does not change the underlying residency requirement. If your account depends on where you legally live, cross-border functionality alone does not solve the problem for people who relocate.

For people living abroad, that distinction matters.

For now, if you move between countries or live semi-nomadic, the fintech banks still feel one step ahead.

Top 7 FAQs for Wise and Revolut Cards

Based on the most common internet queries, here are the top seven questions users ask about traveling and spending with these cards, complete with verified answers from their official help centers:

1. Do I need to convert my money before I travel? No. Both platforms feature auto-conversion technology. If you do not have the local currency pre-loaded in your account, the card will automatically convert the necessary amount from your home currency balance at the exact moment of purchase.

2. What exchange rate do these cards actually use? Wise strictly uses the live mid-market exchange rate (the one you see on Google) and adds a small, clearly stated fee (typically around 0.4% to 1%). Revolut uses its own real-time competitive exchange rate, which is fee-free during weekdays up to your plan’s limit, but applies a 1% weekend markup for users on the standard free plan.

3. How do international ATM withdrawals work? Wise provides two free ATM withdrawals per month up to a total of $100 USD (or equivalent), after which a $1.50 + 2% fee applies. Revolut’s free plan allows up to $400 USD (or £200) per month without platform fees, while premium tiers increase this fee-free limit up to $2,000 USD per month. Both companies warn that third-party ATM operators may still charge their own local machine fees.

4. Will my card work in every country? Because both cards are issued on the Visa and Mastercard networks, they are accepted by millions of merchants worldwide. However, neither card will work in heavily sanctioned regions, including Russia, Cuba, Iran, North Korea, Syria, and Belarus.

5. How long does it take to get a physical card? Standard shipping for a physical card takes between 1 to 3 weeks depending on your location. However, you do not have to wait to start spending; both Wise and Revolut issue a virtual card instantly upon account approval, which can be immediately added to Apple Pay or Google Pay for contactless mobile payments.

6. Should I choose to pay in my home currency or the local currency at the terminal? Both official help centers explicitly warn customers to always choose the local currency when a card terminal or ATM asks. If you choose your home currency, the terminal uses “Dynamic Currency Conversion” (DCC), allowing the local merchant’s bank to apply heavy markups. Choosing the local currency forces the transaction through Wise or Revolut’s much better exchange rates.

7. What do I do if my card gets lost, stolen, or compromised abroad? You do not need to call a bank branch. Both apps allow you to instantly “freeze” your card with a single tap, which immediately blocks all unauthorized transactions. If you find the card later, you can unfreeze it just as easily. If it is permanently lost, you can cancel it and generate a brand-new digital card instantly.

If you already have online banking app on your phone, check out these esential travel applications, maybe you missed an important one.