When my partner and I moved to Malta for three years, the first real headache wasn’t the heat or the driving on the left — it was our Danish bank. Every euro transaction triggered a foreign currency fee, every international transfer needed a desktop login and a card reader, and customer support was only useful during business hours in Copenhagen. We needed an alternative that was reliable, trusted, and actually built for people living between countries. Martin had been reading about both Wise and Revolut and decided to open accounts with both. I ended up with Revolut, and it quickly became my favorite payment method.

The small things mattered first. I designed my own physical card in the app with a fries emblem on it — not plastic but a pinkish metal, heavier and nicer to hold than any card I’d owned before. It arrived in 3-5 days at a remote address in Malta, which surprised me. Then I started using it. Sending money to friends and family in Denmark or to a contributor in another country took a few seconds and a few taps in the app, instead of the 2-minute desktop ritual my traditional bank still required for a single transfer.

Later, I realized my plan came with perks I hadn’t even checked — airport lounge discounts, travel insurance on booked flights, free subscriptions to magazines and podcasts, and a handful of things I still haven’t gotten around to using. We’re now considering opening a Revolut business account too — I recently spoke with an Irish electrical engineer who runs his company through Revolut Business and has had zero issues with it.

Here’s our Locals Insider review of Revolut, the digital banking app I now use daily like 50+ million others (based on the number of app downloads) — from groceries and massages to international transfers. I also get my salary to Revolut and can easily top up my balance when I spend it too fast, simply by moving money from my Danish bank to the Revolut card.

Introducing Revolut, More Than Online Bank

Revolut launched in July 2015 in London, founded by Nikolay Storonsky, a former Credit Suisse and Lehman Brothers trader, and Vlad Yatsenko, a Ukrainian software engineer with a background at major investment banks. The initial premise was narrow but powerful: a prepaid Mastercard that converted currencies at the interbank rate, with no markup. For travelers used to losing 3-5% on every foreign card transaction, it was an immediate hit.

The product line expanded rapidly. By 2017, Revolut had introduced premium subscription tiers. By 2018, crypto trading. By 2020, US launch and stock trading. By 2024, the high-end Ultra tier and the RevPoints rewards system. And by March 2026, full UK banking authorization — the most significant single milestone in the company’s history, unlocking lending products, mortgages, credit cards, and FSCS-protected deposits up to £85,000 per person.

What sets Revolut apart in 2026 is the breadth of features bundled into one app. Multi-currency holding and spending, international transfers, a Mastercard or Visa debit card, virtual and disposable cards, savings vaults, sub-accounts for budgeting, crypto and stock trading, travel insurance on paid tiers, airport lounge access, eSIM data plans, hotel and experience booking, joint accounts, kids’ accounts, and a loyalty points scheme that converts directly to airline miles. The trade-off is that to access most of the genuinely useful features beyond basic spending, you need a paid subscription — and the subscription model is where Revolut earns most of its consumer revenue.

The company is also pursuing a US national bank charter from the OCC, applied for in early March 2026, which would bring full deposit insurance to American customers and unlock the same lending products UK customers now have access to.

How Does Revolut Work?

Revolut works as a mobile-first financial app with a debit card linked to a multi-currency account. After downloading the app and completing a few minutes of identity verification, you get a personal account in your local currency (USD, GBP, EUR, DKK, etc.), and you can open additional currency balances with one tap.

Conversions happen at the interbank exchange rate during weekdays, with a 1% markup on weekends across all plans (a recent tightening — Metal and Ultra used to be exempt). The free Standard plan caps you at €1,000 per month in currency exchanges, with a 1% fair-usage fee above that. Paid plans raise or remove the cap.

Spending with the Revolut card works in 150+ countries with no foreign transaction fee on amounts up to your plan’s monthly exchange limit. ATM withdrawals are free up to a monthly amount that varies by plan, with a 2% fee on excess. Transfers between Revolut users are free and instant. International bank transfers go through SWIFT or local rails (SEPA in Europe, Faster Payments in the UK, ACH in the US), with the fee depending on destination country and plan tier.

How to Use Revolut in 5 Steps

Here’s how the most common Revolut actions actually play out in practice.

1. Pay in a shop, restaurant, or café (physical card or phone). Open Apple Pay or Google Wallet, or just tap your physical Revolut card. At the terminal, if asked “pay in local currency or your home currency?” — always choose the local currency. Letting the terminal convert (Dynamic Currency Conversion) typically adds 5-10% to the cost. The app sends an instant push notification with the exact amount, exchange rate used, and your running monthly spend.

2. Withdraw cash from an ATM abroad. Insert your card, enter your PIN, and when the ATM asks whether to convert to your home currency, always decline — choose to withdraw in the local currency and let Revolut handle the conversion at the interbank rate. The first €200-£200 of monthly ATM withdrawals are free on the Standard plan, with higher limits on paid tiers. Decline any ATM that asks for a separate “conversion fee” upfront — these are usually independent operators like Euronet that add 10-15% to the rate if you let them convert.

3. Pay online with the Revolut card or Revolut Pay. Two options here. The simpler route: enter your card details (or use a virtual card from the app for added security) at checkout, exactly like any other debit card. The smarter route at supported retailers: look for the Revolut Pay button at checkout, click it, confirm the payment with biometric authentication in the app, and you’re done in one click. Revolut Pay also earns you double RevPoints on the purchase, doesn’t share your card details with the merchant, and gives you Buyer Protection coverage. For one-time purchases on sites you don’t fully trust (subscription trials, unknown sellers), tap “Disposable virtual card” in the app first — it generates a new card number for that single transaction, then self-destructs.

4. Send money to friends or family. If they have a Revolut account, send via username or phone number — it’s free, instant, and no IBAN required. Open the app, tap Send, search for the contact, enter the amount, confirm. The recipient sees it land in their app within seconds. If they don’t have Revolut, the same flow works for any standard bank account: enter the recipient’s name and account details (IBAN for Europe, account + routing number for the US, sort code for the UK), choose the amount, and Revolut shows the fee and arrival estimate before confirming.

5. Send an international transfer to a bank account in another country. Tap Payments → New Payment → New Recipient. Choose the destination country and the currency you want the recipient to receive. Enter their IBAN, SWIFT/BIC code, or country-specific bank details. Revolut shows you the exchange rate, the fee (often a few euros for major corridors, more for exotic currencies), and the estimated arrival time before you confirm. Most transfers within Europe (SEPA) arrive same-day or within 1 business day. Transfers to USD, GBP, or major Asian currencies usually arrive within 1-2 business days. You can also schedule recurring transfers — useful if you’re paying rent abroad or sending regular money home to family.

The whole flow is genuinely faster than a traditional bank — most actions take under 30 seconds once you’ve used the app a few times.

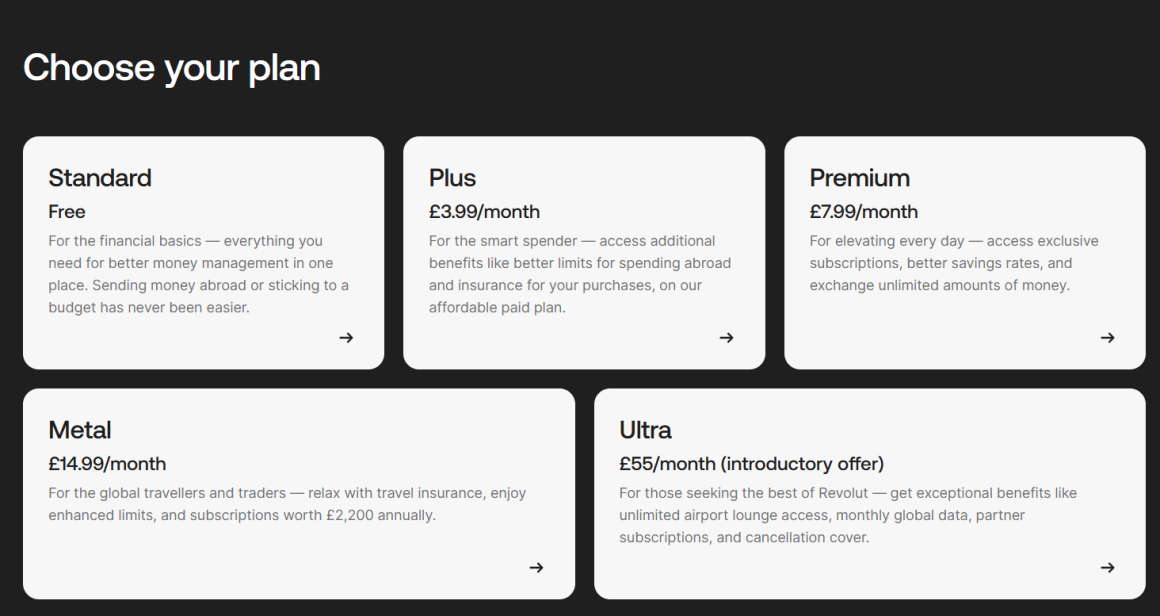

Revolut Plans & Pricing: How Much Does It Cost?

Revolut now offers five plan tiers in the UK and EU (the US has fewer — Standard, Premium, and Metal only, as of mid-2026). Pricing varies slightly by country but the structure is consistent:

Standard — Free. One fee-free ATM withdrawal up to €200/£200 per month, €1,000 monthly currency exchange limit (1% fair-usage fee above), basic plastic debit card, crypto and stock trading available with standard fees, joint accounts, vaults, budgeting tools. Best for occasional travelers, light users, or people testing the platform.

Plus — Around £3.99 / €3.99 per month. Everything in Standard, plus purchase protection up to €1,000, two free ATM withdrawals per month, 0.5% fair-usage fee above the €1,000 currency exchange limit, and a Plus card design. Best for occasional travelers who want basic purchase protection.

Premium — Around £7.99 / €9.99 / $9.99 per month. Everything in Plus, plus higher free ATM limit (€400/£400 monthly), overseas medical insurance, flight delay and lost baggage cover, winter sports insurance, disposable virtual cards, and discounted LoungeKey or DragonPass airport lounge access. Best for regular travelers and freelancers with international clients.

Metal — Around £14.99 / €16.99 / $16.99 per month. Everything in Premium, plus higher ATM limit (€600/£600 monthly), the metal debit card (reinforced steel — this is the tier I personally use), up to 1% cashback outside Europe (capped at the monthly fee), purchase protection, car rental excess insurance, and higher interest on Vaults savings. Best for frequent travelers, digital nomads like we are, and anyone who’ll use the perks regularly.

Ultra — Around £45 / €55 per month. Everything in Metal at higher tiers, plus Cancel For Any Reason travel insurance, comprehensive worldwide travel insurance, eSIM data plan included, free airport lounge access for the Ultra holder plus one guest, partner brand subscriptions bundled (Financial Times, Headspace, Tinder Gold, and others — varies by country), and 1 RevPoint per £1/€1 spent (the highest earning rate). Best for expats, very frequent travelers, and people who’d otherwise pay separately for premium travel insurance and airport lounge memberships.

US-based readers should note that pricing differs and the Plus and Ultra tiers are not currently available in the United States. UK and EU customers can also pay annually for a small discount (typically 10-15% off versus monthly billing).

Can You Use Revolut in the USA?

Yes — Revolut launched in the United States in 2020 and now has around one million US customers, but the US version differs from the EU and UK product in a few important ways.

Revolut isn’t yet a fully licensed US bank. It operates through a partnership with Lead Bank in Kansas City, which holds the actual deposits and provides FDIC insurance up to $250,000 per customer. In daily use, this is invisible — you get a routing number, can receive direct deposit, and spend with the debit card exactly like any normal US bank account.

That’s set to change in 2027. On 5 March 2026, Revolut filed for a US national bank charter with the OCC and FDIC, with the new entity to be called Revolut Bank US, N.A., headquartered in Stamford, Connecticut. Once approved, it will unlock personal loans, mortgages, credit cards, high-yield investment accounts, direct access to Fedwire and ACH payment rails, and FDIC insurance through Revolut itself rather than through Lead Bank.

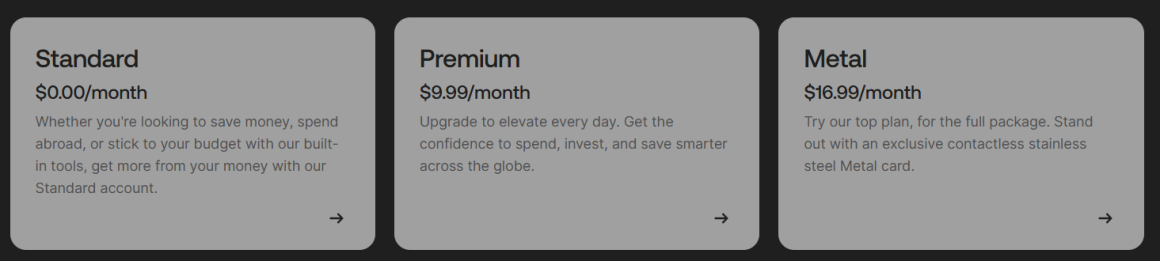

US customers currently have access to three plans only — Standard (free), Premium ($9.99/month), and Metal ($16.99/month). The Plus and Ultra tiers available in Europe haven’t launched in the US yet. Available features include multi-currency holding and spending in 150+ countries, ATM withdrawals with monthly free limits per plan, instant transfers to other Revolut users, international transfers via SWIFT, stock trading through Revolut Securities (a FINRA/SIPC member that issues 1099 forms), crypto trading, virtual and disposable cards, joint accounts, and savings vaults.

The features US customers don’t yet have are worth knowing: the RevPoints rewards program is currently EU and UK only, eSIM data plans aren’t available, and there are no personal loans, mortgages, or credit cards until the bank charter clears. International transfer fees can also be slightly higher than European equivalents because they often route through SWIFT rather than local payment rails like SEPA.

The practical takeaway for our US readers: Revolut works very well for everyday spending, ATM withdrawals abroad, currency holding, and multi-currency travel. Your money is FDIC-insured through Lead Bank, the app experience is identical to the European version, and the Metal card with cashback genuinely earns its keep for frequent travelers. If pure international transfer pricing matters most, Wise still typically wins on raw exchange rates. If you want an all-in-one app experience and are willing to wait for the full US feature set that will come post-charter, Revolut is the stronger long-term bet.

RevPoints: Revolut’s Rewards System

Launched across Europe in June 2024 and rolled out to the UK in 2025, RevPoints is Revolut’s answer to airline miles and credit card reward programs. Unlike most reward schemes, RevPoints runs on a debit card, which means no credit check, no interest charges, and no minimum spending requirement.

How many points you earn depends entirely on your plan tier. Standard and Plus customers earn 1 point per £10/€10 spent. Premium customers earn 1 point per £4/€4. Metal customers earn 1 point per £2/€2. Ultra customers earn 1 point per £1/€1.

Additional ways to earn include 2-5x points when booking via Revolut Stays (1.8 million properties across 200+ locations) or Revolut Experiences, 50 points per €1 in spare-change round-ups, and bonus points for in-app challenges like setting a savings goal, referring a friend, or completing a budget target.

The redemption options are where RevPoints actually delivers value. Points convert 1:1 into airline miles in major programs — most notably Flying Blue (Air France/KLM), Avios (British Airways, Iberia, Aer Lingus), and a growing list of partners. They can also be redeemed for discounts on Stays bookings (5,000 points roughly equals €100 off a hotel), shopping vouchers, or applied at online checkout through Revolut Pay for direct discounts.

For a deeper dive into how to use RevPoints effectively, the YouTube channel Money Unshackled covered the full system in their explainer Revolut RevPoints: Everything You Need To Know in 2026, which breaks down the math on whether Ultra’s premium price is recouped through the higher point earn rate for frequent spenders.

Revolut Cards: Plastic, Metal, Virtual & Disposable

Every plan includes at least one physical card and unlimited virtual cards. Card types include:

Plastic debit cards — the default for Standard, Plus, and Premium customers. Standard contactless Mastercard or Visa, depending on country.

Metal cards — exclusive to Metal subscribers. Brushed-steel construction, weighs noticeably more than a typical card, available in multiple finishes (rose gold, silver, black, space grey, and several limited-edition options). You can also design your own with a custom emblem or image through the app, which is what I did. Cosmetic rather than functional, but the heft and finish are genuinely nicer than any traditional bank card.

Ultra cards — the most exclusive tier, with an even heavier construction and unique design language. Limited to Ultra subscribers.

Virtual cards — unlimited on all plans. Created instantly in the app, addable to Apple Pay and Google Wallet, useful for online subscriptions or one-time purchases.

Disposable virtual cards — available on paid plans (Plus and up). Each transaction generates a new card number, then the card “self-destructs,” providing strong protection against subscription scams or data breaches. Useful for trial signups on sites you don’t fully trust.

Replacement card fees vary: standard plastic replacement is usually free to £5; replacing a Metal or Ultra card can cost £20-70 depending on the design. Physical card delivery times are surprisingly good — mine arrived in 3-5 days to a remote address in Malta, and reports from users in other markets suggest similar speeds for most EU countries, the UK, and the US.

Reviews & Ratings: Can I Trust Revolut with My Money?

Revolut’s regulatory and trust position improved substantially with the March 2026 UK banking license. UK customers’ eligible deposits in Revolut Bank UK Ltd are now FSCS-protected up to £85,000 per person — the same coverage as deposits at HSBC, Lloyds, or Nationwide. EU customers have similar protection through Revolut Bank UAB, which is licensed in Lithuania and covers deposits up to €100,000 under that country’s deposit guarantee scheme. US customer balances are FDIC-insured through partner banks.

Across both app stores, ratings are very strong:

App Store rating: 4.7/5.0 (around 70,000 reviews) Google Play Store rating: 4.7/5.0 (around 4 million reviews)

A representative Google Play Store review reads: “As a traveler, this app and card is so handy and useful. Being able to create one-use cards means I don’t have to worry. The one time I had an issue with my card, Revolut was fast at rectifying the situation, sending me a new physical card and canceling the old one” — Benjamin Richards.

Common complaints across both stores cluster around two themes: occasional account freezes during source-of-funds verification (Revolut’s compliance checks have tightened sharply since 2023), and customer support being app-chat-only with no phone line for most issues. The first is genuine and can be stressful if it happens while you’re abroad with no cash backup. The second is industry-standard for fintechs but worth knowing if you expect traditional bank-style support.

Locals Insider tip: Before you travel, generate a PDF account statement covering the last 6-12 months and save it to your phone. Combined with a screenshot of your most recent tax return and a recent client invoice or salary slip, this is the documentation Revolut typically asks for during a source-of-funds check. Having it ready turns a 48-hour disruption into a 30-minute upload.

For longer-form perspectives from full-time travelers, the YouTube review I Spent 5 Years Using Revolut And Here’s My Honest Review covers the real-world experience across multiple country moves, and digital nomad blogger Two Tickets Anywhere has a written equivalent at twoticketsanywhere.com that’s worth reading if you’re weighing the Metal upgrade specifically.

Revolut & Taxes: What Travelers and Digital Nomads Need to Know

This is the section most reviews skip, but it’s genuinely important for anyone moving money across countries with Revolut.

Revolut does not automatically issue an end-of-year tax statement. You have to generate one yourself. In the app, go to Profile → Documents → Bank Statements, select your account and date range, choose PDF or CSV format, and tap Generate. The statements include income, expenses, deposits, withdrawals, and currency exchanges in detail. This is essential for tax filing in most jurisdictions.

US citizens and green-card holders need to be aware of FBAR. If the combined balance of all your foreign financial accounts — including any Revolut Bank UAB (EU) or Revolut Bank UK Ltd accounts — exceeds $10,000 at any point during the year, you must file FinCEN Form 114 separately from your regular tax return. The threshold is cumulative across all foreign accounts, not per account. Penalties for non-filing start at $10,000 per violation and rise significantly for willful violations. The US Revolut Securities entity will issue 1099 forms for investment activity, but standard Revolut account interest, conversions, and balance information does not generate automatic IRS reporting.

For crypto transactions on Revolut, tax-reporting tools like Koinly, CoinLedger, and CoinPanda accept CSV uploads of Revolut crypto transaction history. Revolut doesn’t currently offer API connections to these tools, so the workflow is: download CSV from Revolut, upload to your chosen tax tool, generate the tax forms.

EU citizens should be aware that Revolut Bank UAB reports to the Lithuanian tax authority, which under the Common Reporting Standard (CRS) shares data with other EU tax authorities automatically. Practically, this means your tax office in Denmark, Germany, Spain, or France can request your Revolut account information without notifying you. For most users this is a non-issue (taxes are filed correctly anyway), but it’s worth knowing if you’re trying to figure out tax residency questions.

For UK customers, Revolut now reports under standard UK banking rules following the March 2026 license grant. HMRC has access to the same reporting any other UK bank provides.

For digital nomads weighing tax residency more broadly, the Foreign Earned Income Exclusion for US citizens (around $132,900 for 2026) and various physical presence and bona fide residence tests are worth understanding before optimizing for any specific Revolut setup. Locals Insider isn’t a tax-advice publication and the rules change frequently — always work with an accountant who specializes in expat or digital nomad taxation if you’re earning meaningful income while abroad.

Revolut’s Pros and Cons

The strengths: the most polished mobile banking app on the market, full UK banking license and FSCS protection as of March 2026, multi-currency holding and spending in dozens of currencies, comprehensive features (budgeting, analytics, vaults, crypto, stocks, eSIM, travel insurance), competitive interbank exchange rates on weekdays, the RevPoints program that genuinely competes with airline credit card schemes, strong card security through disposable virtual cards, free joint accounts and kids’ accounts, custom card design options, and growing global coverage including the pending US bank charter.

The trade-offs: the best features sit behind monthly subscription tiers, weekend currency conversion adds a 1% markup on all plans, occasional account freezes during source-of-funds verification can be disruptive while traveling, customer support is in-app chat only for most issues with no phone line, the US version offers fewer features than EU/UK (no Plus or Ultra tier yet), and Wise still typically offers cleaner mid-market exchange rates for pure international transfers without the subscription bundling.

Alternatives to Revolut? Consider Wise

Wise (formerly TransferWise) is the natural Revolut alternative. The core difference: Wise is 100% free to open and use, with no monthly subscription fees on personal accounts. Wise earns its money through transparent transaction fees ranging from about 0.33% to 1.5% per conversion, with the mid-market exchange rate guaranteed (no weekend markup). Revolut, by contrast, makes most of its consumer revenue from subscription tiers, and the best features — high ATM limits, unlimited currency exchange, airport lounges, insurance — require paying for Premium, Metal, or Ultra.

Where Revolut clearly beats Wise: the breadth of bundled features. Wise has no insurance, no airport lounge access, no points program, no crypto or stock trading, no eSIM, and no budgeting analytics beyond basic transaction history. If you want a single app that does everything, Revolut is the answer. If you want the cheapest possible international transfers and don’t need the extras, Wise wins on raw pricing.

The practical pattern Martin and I both follow, and what we see among long-term travelers, freelancers, and digital nomads, is to use both: Wise for receiving payments from international clients, holding currency reserves, and large transfers; Revolut for daily spending, ATM withdrawals abroad, travel insurance, and the points-earning everyday card. The two apps complement each other rather than directly competing, and most experienced travelers eventually hold both.

For more on managing finances while traveling, you might find our guides to Bangkok’s digital nomad neighborhoods, our best travel apps roundup, and our 12 best travel gadgets guide useful starting points.